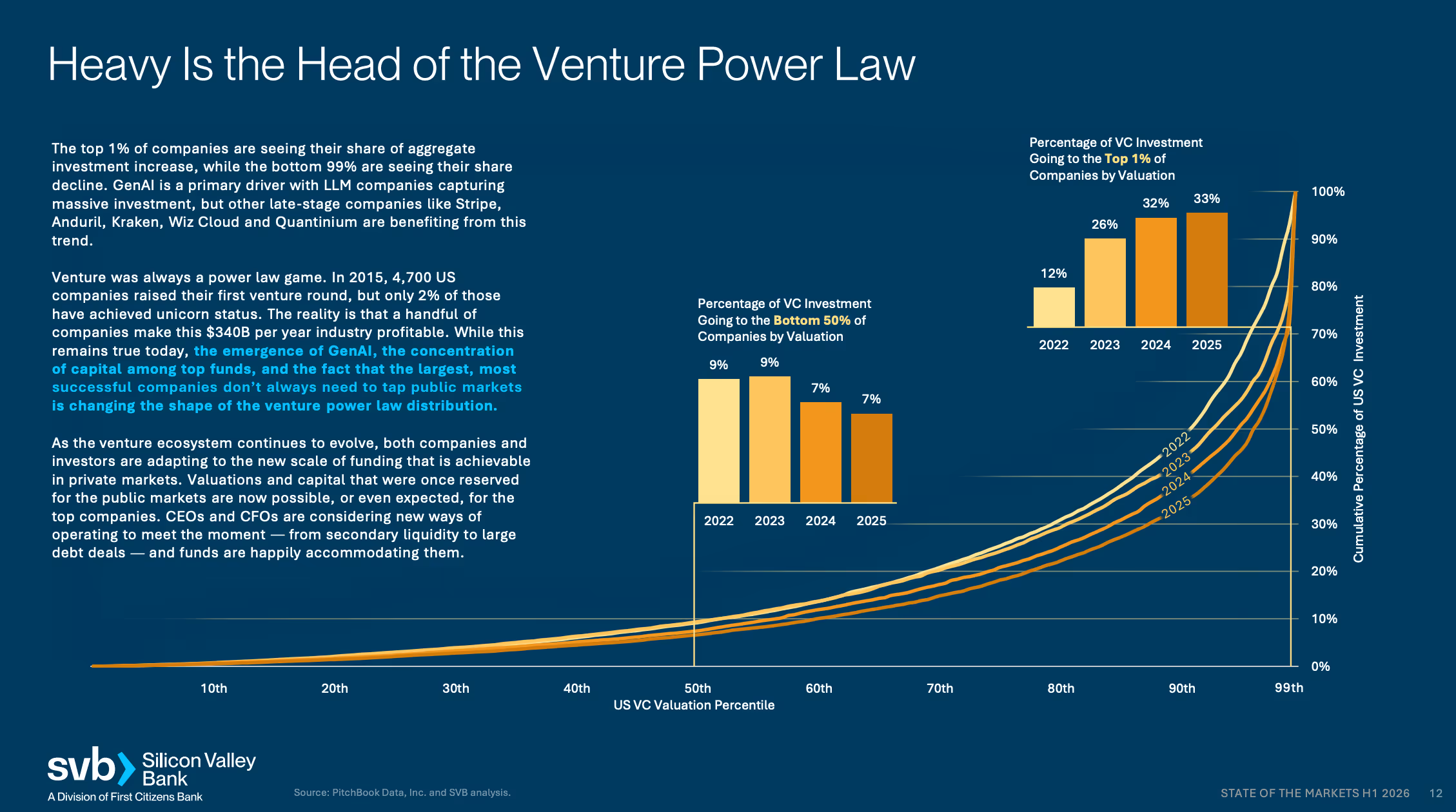

The top 1% of venture-backed companies captured 33% of all VC investment in 2025. Read that again. One percent of companies, one-third of the capital.

Silicon Valley Bank just released their State of the Markets H1 2026 report, and the data had me thinking: does venture capital have a naming problem? When SoftBank writes a $30B check to OpenAI and a first-time founder raises $500K from friends and family, we call both "venture capital." But are they really the same thing?

What Venture Capital Was Built to Do

Let's start with first principles. Venture capital exists as the high-risk, high-return corner of private equity. It was designed to fund innovation too risky for banks and too early for public markets. The model accepts 50-70% failure rates because the winners return 10x to 50x to make up for the losses.

This is why LPs (pension funds, endowments, family offices) allocate to venture. They want uncorrelated returns and access to high-growth companies before they go public. Traditional VC works through portfolio construction: invest in 30-50 companies, take 15-25% ownership, and bet that 2-3 massive wins will return the fund.

The economics run on carried interest (20% of profits), not management fees. You only get paid when your companies exit. High risk, high alignment, high stakes.

That model was built for $500K to $40M rounds into teams with ideas. It was never designed to deploy $500M into a company with $200M in revenue.

Two Different Games Hiding Under One Name

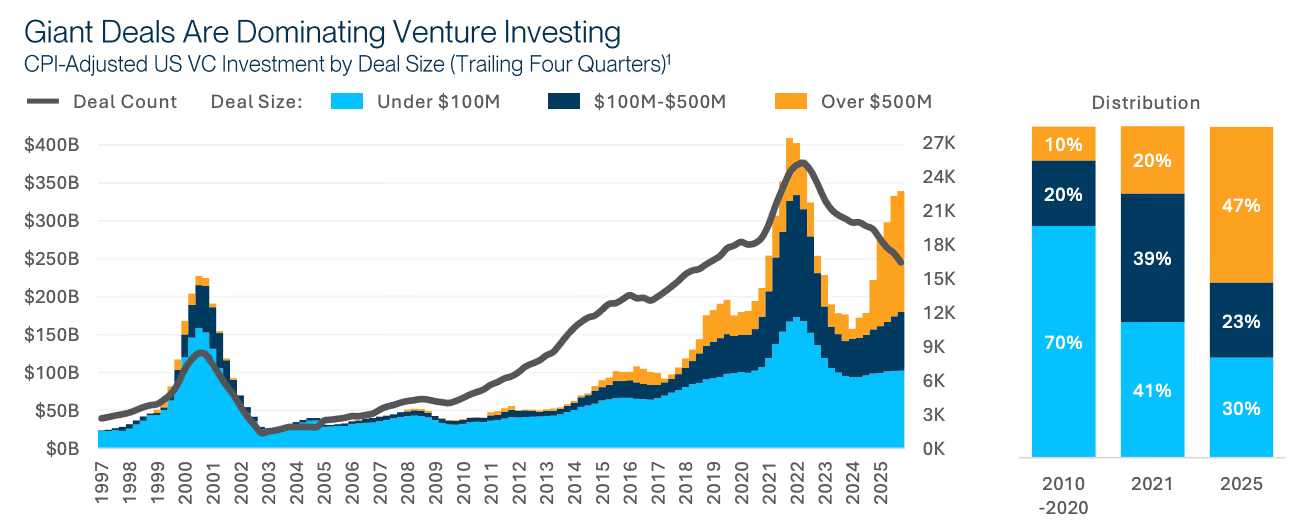

Here's where the data gets interesting. In 2025, US venture investment hit $340B, the second-highest year on record. But deal count dropped 15% from the prior year. More capital, fewer companies. The math only works one way: massive checks into a handful of companies.

Twenty-four companies raised billion-dollar rounds in 2025, compared to 17 in peak-2021. Those 24 deals absorbed roughly $36B. Strip out the billion-dollar rounds from both years, and the story flips: 2025 deployed approximately $304B versus 2021's $324B. When you compare apples to apples, 2025 wasn't a recovery. It was down 6% from the peak. The "growth" in VC came almost entirely from mega-rounds. Meanwhile, the bottom 50% of companies by valuation captured just 7% of total investment, down from 9% in 2022.

Then there's the "$100M seed round" phenomenon. AI companies are raising nine-figure rounds before product-market fit and calling it "seed." Let's compare what that actually means:

Traditional seed: $500K-$3M, 50-70% failure rate, 10x+ return expectations, you're betting on a team and an idea.

"$100M seed": Pre-revenue but capital-intensive, already picked by top-tier funds, 2-3x return expectations, basically growth equity with different branding.

These aren't the same risk profile. They're not even close.

Not only that, but even the unicorns themselves are starting to show a tale of two cities. According to recent PitchBook data, 51.8% of the value of ALL unicorns in 2025 is concentrated among the top 10 unicorns. In 2024 it was 35.6%.

The investor breakdown from SVB tells the story: 4% of investors (roughly 500 firms) are doing $500M+ deals. Meanwhile, 84% of investors (about 11,200 firms) are doing sub-$100M deals. Same industry? Or two industries sharing a name?

The Economics Changed

Platform funds changed the game. When Andreessen Horowitz raises $15B across multiple strategies, the math shifts. At 2% annual management fees, that's $300M in fees every year. When you're generating $300M annually just for showing up, you're running an asset management business, not a traditional venture firm.

Fee-driven economics incentivize different behavior than carried interest economics. You need to deploy capital fast and at scale. Writing 150 checks of $2M is operationally harder than writing 15 checks of $200M. The math pushes you toward bigger, later, safer bets.

This isn't a criticism. It's just a different business model. But we're using the same words to describe it.

The Returns Tell a Different Story

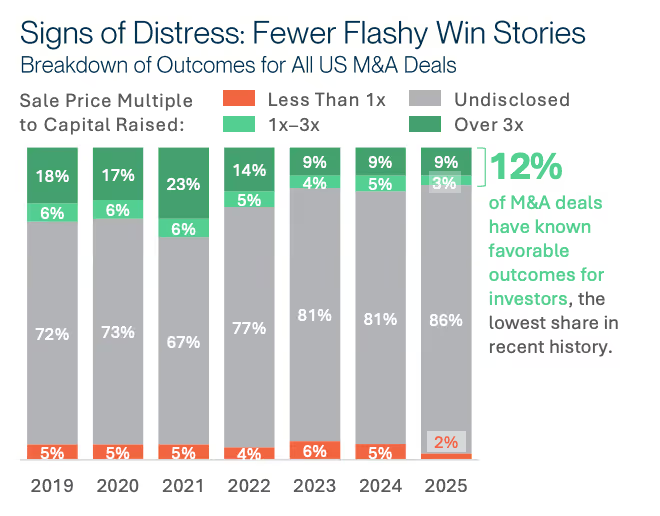

Here's the part that should worry everyone: most exits in 2025 didn't return capital to investors.

Only 12% of M&A deals had known sale prices greater than the capital the companies had raised. The other 88%? Either returned less than 1x or had undisclosed prices (which usually means bad news). M&A has become portfolio management, not liquidity events.

IPOs aren't much better as a relief valve. The median 2025 IPO had $250M in revenue and was 12.5 years old. But here's the kicker: half of the 857 US venture-backed unicorns already have more than $800M in revenue. They're bigger than typical IPO candidates but staying private because they can. There's $4.4T locked up in these private unicorns, with secondary markets providing liquidity to maybe the top 10% of companies.

If you're an LP who allocated to "venture capital" expecting uncorrelated, high-return outcomes, what happens when half the capital in that bucket is going into late-stage, lower-risk growth equity? The risk-return profile of the entire asset class shifts. And that matters when you're managing pension fund allocations or endowment portfolios.

Traditional VC promised 3x-5x fund returns with massive variance. Late-stage growth equity promises 1.5x-2x with less risk. Those require completely different allocation strategies. But we're calling them both "venture" and aggregating the data.

So What Do We Call This?

Two paths forward, and I'm genuinely not sure which is right.

Option 1: Bifurcate the category. Create new language. Maybe it's "Venture Capital" for sub-$50M rounds with carried interest economics and 10x return expectations versus "Platform Equity" or "Pre-IPO Growth" for $100M+ rounds with fee-driven economics and 2-3x expectations. Separate the data, separate the benchmarks, separate the LP allocation buckets.

Option 2: Accept the evolution. Maybe venture capital simply grew up. The Sequoias and Andreessens of the world now operate across the entire lifecycle from seed to IPO. The economics changed, the scale changed, but the category stayed the same. Is that wrong, or just different?

The practical problem is this: when SVB publishes that $340B was deployed in "venture capital" while the median seed company can't graduate to Series A (only 3% make it in 12 months, down from 20% historically), something doesn't add up. The story those numbers tell depends entirely on which version of "venture" you're talking about.

The Question Worth Answering

Does venture capital have a naming problem, or has the game changed so fundamentally that we need a new framework?

When is a seed round not a seed round? When does venture capital become something else? If the top 1% captures 33% of capital, are we measuring two industries or one?

And for the LPs writing the checks: does it matter what we call it, or only what it returns?

The industry grew too fast to stop and rename things. But when a $30B OpenAI round and a $500K friends-and-family seed are both "venture capital," maybe it's time we had the conversation.

.avif)